How we see the personal care industry in the next 5 years

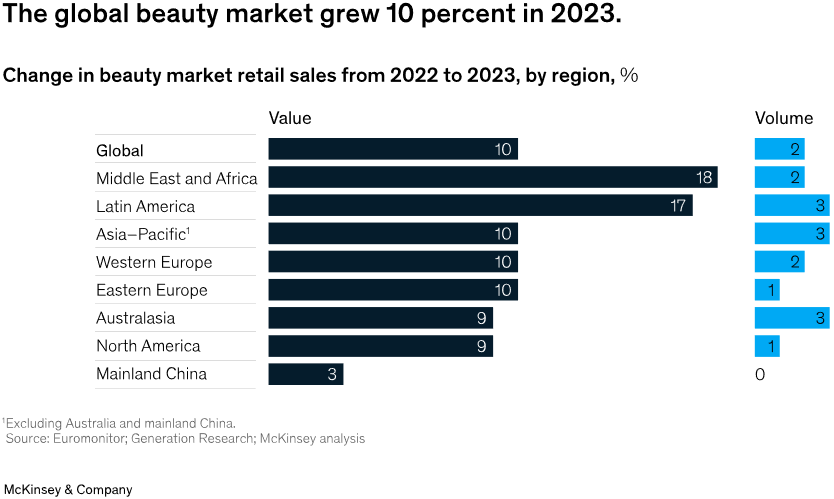

In 2023, global beauty market retail sales grew to $446 billion, up 10 percent from 2022. In the year, the industry—comprising fragrance, makeup, skin care, and hair care—beat expectations and outperformed other consumer sectors, such as apparel.

In 2023, price increases across tiers drove much of the growth in beauty, although some consumers—particularly those in emerging markets such as the Middle East—also indicated a desire to spend on higher-priced categories. One challenge beauty players will face includes understanding why consumers may be trading down and where their appetite for luxury products is growing, given that we see a mix of both trade-down and trade-up behaviors in the market.

Mass beauty, the least expensive segment, represented 48 percent of the beauty industry’s value in 2023. The value of the mass tier grew 10 percent during this period, in part because a share of consumers (up to 20 percent) in mature markets such as the United States and Europe said they had switched to cheaper brands. Masstige, the next pricing tier up, grew 8 percent in 2023. We expect the mass segment to grow by 5 percent annually through 2028 and the masstige segment to grow by 6 percent over the same period.

Today, inflation is cooling in major markets such as Europe and United States, giving beauty players an opportunity to reset and focus on pursuing sustainable growth strategies over the next several years.

A McKinsey survey outlines the beauty sector’s performance in 2023 and the forecasts through 2028.

REGIONAL GROWTH

The beauty market’s 10 percent growth in 2023 exceeded industry forecasts across nearly all regions:

The Asia–Pacific region, excluding China and Australia, remained the largest region by retail sales in 2023, growing at a 10 percent rate over the previous year. India, which also grew at a 10 percent rate year over year, was a bright spot in the region (with 4 percent volume growth and 6 percent price growth). As reflected in our regional survey data, India was home to the highest number of consumers who indicated a willingness to spend more on beauty products in 2023 and 2024. This was true across all income groups; in fact, low-income consumers in India were the only low-income consumers in our survey to say they intended to spend more on beauty products through the second quarter of 2024.

In North America, which today accounts for 20 percent of the overall beauty market, retail sales grew by 9 percent year over year. Europe, another mature beauty market, grew 10 percent from 2022 to 2023. Growth in the Middle East and Africa region and Latin America reached 18 percent and 17 percent, respectively, year over year, both exceeding industry expectations.

In 2023, price increases drove year-over-year growth in the sector, while global volume across geographies only grew 2 percent over the same period. Given that prices rose across segments, some consumers in the United States, for example, made trade-offs between discretionary purchases and prioritized price and value in their personal-care purchases. These consumers traded down—opted for smaller quantities or lower-priced goods or retailers—or delayed purchases altogether, which contributed to low volume growth (1 percent). We expect price increases to stabilize now that inflation is cooling across major markets, such as the United States.

China’s growth in 2023 was different from that of other regions globally. China’s beauty market grew only 3 percent—driven entirely by price growth. This growth rate was in line with the country’s broader economic performance but weaker than industry expectations. A range of macroeconomic factors, low consumer confidence, and widespread discounting and promotions (which encouraged consumers, in search of lower prices, to delay purchases) all contributed to the performance of China’s beauty sector. Looking ahead, while middle- and high-income consumers in the country said they intend to spend more on beauty products through 2024, low-income consumers said they intend to spend less on beauty compared with survey responses from earlier in the year. This reduced spending could impact on the sector’s performance through the end of the year.

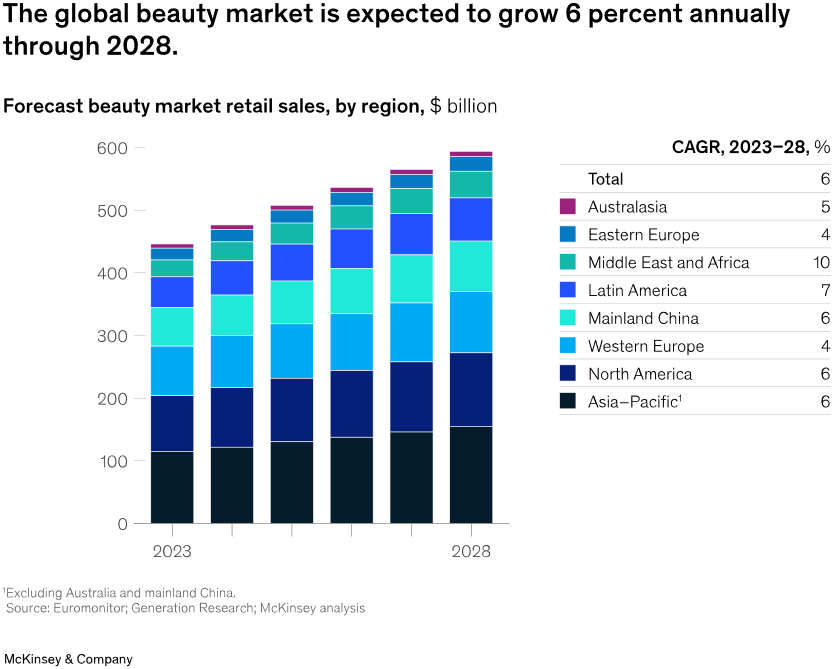

By 2028, we expect the beauty sector to reach $590 billion, with an annual growth rate of 6 percent (Exhibit 2). In mature markets, such as the United States and Europe, we estimate that both price and volume growth will be in the low single digits.

We expect the Asia–Pacific region, excluding China and Australia, to grow 6 percent annually, representing nearly one-quarter of the total market, which is consistent with its share today. Here, we anticipate that volume growth will outpace price growth (we estimate 4 percent volume growth and 2 percent price growth).

Despite the wider economic challenges facing China in the near term, we expect to see 6 percent annual growth in the country through 2028. Gen Z and millennials are likely to drive this growth, as are higher-income consumers. The “lipstick effect”—when consumers continue to spend on modest luxuries, such as lipstick, when the economy weakens—has contributed to some growth in China in 2024. Beauty spends through 2028, therefore, will be somewhat dependent on how its economy evolves. We will likely see lower volume growth, given the challenges in the region, while price growth will be in line with expected inflation.

Finally, we anticipate seeing the highest annual growth rate in the Middle East and Africa (10 percent) over the next four years. Price mix increases will most likely outpace volume growth here more than anywhere else in the world, as consumers continue to demand premium products.

The category future best performers

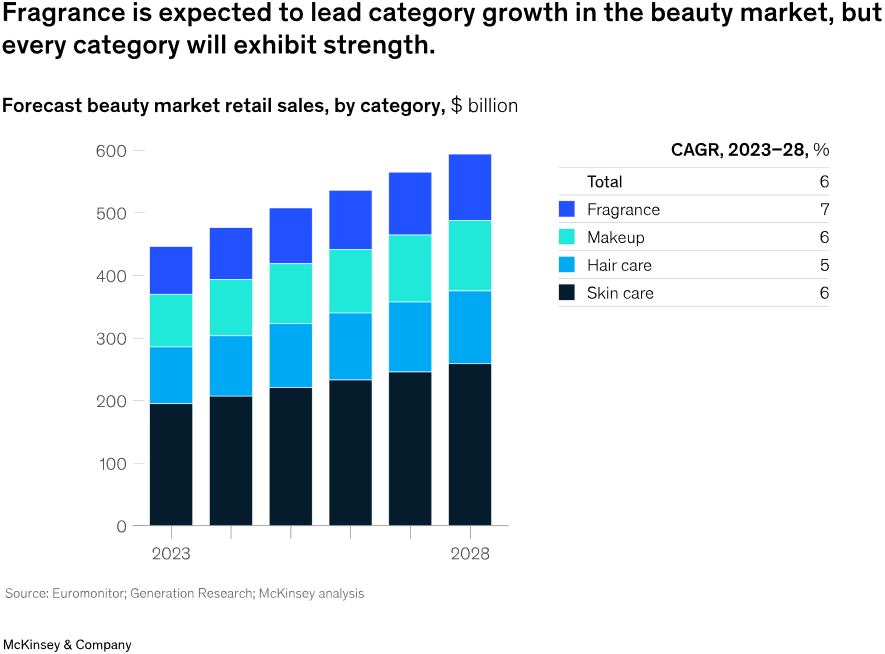

Skin care—the sector’s largest category, accounting for 44 percent of the market—grew 6 percent in 2023, in line with projections (Exhibit 3). Once again, price increases in the Middle East and Africa, Latin America, and to a lesser extent, in Europe and North America, drove much of this growth. (It’s worth noting that shifts in large, mature markets such as Europe and North America can have a larger impact on the global industry compared with shifts in places like the Middle East and Africa and Latin America, despite high relative price growth in these areas.) In China, growth in the skin care category was mostly flat.

Over the next four years, we expect the skin care category to grow at an annual rate of 6 percent, with a greater equilibrium between volume and price growth. This will likely be the case as more consumers across age groups (Gen Z and Gen Alpha among them) continue buying into the category. (To a lesser extent, men may also drive volume growth in skin care). We also anticipate that new, buzzy ingredients—neuropeptides, for example—will continue to fuel growth in skin care over the next few years. Meanwhile, the “skinification” of hair—the introduction of elaborate routines and specialized products to the hair category, as has been the case in skin care—helped propel growth in hair care in 2023 and is expected to do so over the next five years. As for price-related growth, we anticipate price increases to be mostly tied to the development of more sophisticated, and therefore more expensive, products.

Despite being the smallest category in beauty, representing just 17 percent of the market, fragrance posted the highest growth (14 percent) in 2023. The category is likely to continue exhibiting strong growth, especially in the Asia–Pacific region, where it currently represents around 5 percent of the total market (compared with 17 percent in North America and 27 percent in Europe). Globally, we expect price growth to outpace volume growth in fragrance, which the expansion of the luxury price tier will help drive.

The Asia–Pacific region offers beauty players the greatest opportunity to expand volume growth over the next few years. In more mature markets, such as Europe, volume growth is also projected to remain healthy.

Niche fragrances—those that appeal to “in the know” consumers without relying on celebrity endorsements—are expected to be among the biggest drivers of growth within this category. Here, craftsmanship and ingredients play an important role in brands’ positioning and storytelling. As the niche fragrance category thrives, larger beauty players will continue to invest in or acquire these emerging brands. In doing so, they must carefully scale a niche brand without alienating the consumers who helped propel its early growth. As one global beauty executive said recently, “Barriers to entry may be coming down, but barriers to scale are only going up.”

Finally, makeup has recovered from its pandemic-era contraction. Retail sales in 2023 surpassed 2019 levels for the first time. We expect the Asia–Pacific region, as well as the Middle East and Africa, to propel growth in this category through 2028 as consumer purchasing power increases and specialty beauty retailers improve their penetration in these markets. Although we anticipate seeing some volume growth in makeup, this category is becoming more competitive than ever, requiring players to consistently innovate and clearly define their value proposition to consumers. Beauty players can innovate in cosmetics by offering more skin care–infused products, products that are created more sustainably, and more functional packaging.

Growth in stores and online

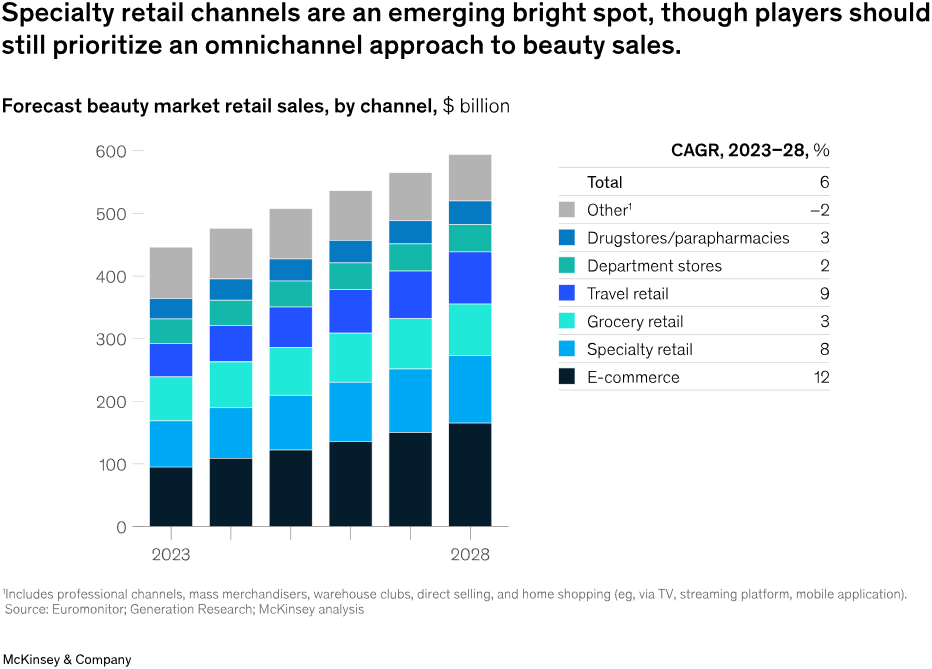

Online sales channels accounted for much of the beauty industry’s growth at the height of the COVID-19 pandemic. While online sales growth was still strong in 2023, growth in physical channels accelerated during this period.

Global sales at specialty beauty retailers—those that cater specifically to beauty consumers—grew 14 percent last year. (North American and European specialty beauty retailers propelled this growth.) In 2023, these retailers became a destination for discovery and in-store beauty services. An important distinction between specialty beauty retailers and department stores continues to be the “open sell” concept, favored by younger consumers, in which shoppers can test and compare products themselves without relying on a store associate who may be behind a beauty counter. To appeal to younger shoppers, these retailers prominently display products that are trending online to help bridge the gap between the online and in-store experience. To that end, best-in-class specialty retailers also continue to cultivate engaged social media communities.

Despite growing the least among the physical channels, department stores still achieved 7 percent growth globally, buoyed by growth in Europe and the Middle East. Drugstores and pharmacy beauty sales also grew in 2023 (9 percent), albeit at a lower rate than specialty retail sales (14 percent).

While e-commerce firmly represents the largest single channel for beauty globally, the channel grew only 8 percent. The Middle East and Latin America saw stronger e-commerce growth than other regions. In these markets, investments in digital infrastructure, logistics, and payments, as well as growing consumer internet penetration and mobile-device usage, led to higher e-commerce penetration.

We see that the investments retailers have made in improving their in-store shopping experience—creating visually appealing spaces with an added focus on Gen Z consumers, for example—have encouraged shoppers to return to physical stores. However, the in-store experience must seamlessly extend to the online realm. Successful retailers cultivate communities across social media and their own websites to ensure shoppers remain in the retailer’s ecosystem, even after they’ve left the store. Consumers will continue to conduct price comparisons both online and in-store to look for the greatest savings, making a sophisticated yet clear pricing strategy pivotal for success.

Conclusion

The beauty industry has proven resilient in the face of economic turbulence, but the era of de facto price-fuelled growth is over. To build sustainable momentum, best-in-class beauty brands will need to create real value from product differentiation, supported by greater productivity. Executives should focus on becoming more attuned to shifting consumer preferences while doubling down on their brands’ and products’ unique value propositions. Agility and speed to market—which the use of new technologies such as AI and generative AI can enable—will distinguish the best from the rest, as will the ability to cultivate strong communities of loyal customers.

By: Massimiliano Morpurgo